Need a new dividend stock you know you can count on? The usual suspects like Coca-Cola and Procter & Gamble remain solid options. You may have better luck, however, with a dividend stock that has an equally strong track record that’s a bit off the beaten path. That’s Dividend King Illinois Tool Works (ITW +0.14%).

Built to last

Contrary to a common assumption, Illinois Tool Works doesn’t manufacture typical hand tools like hammers and drills. Rather, automobile parts, commercial-grade cooking, industrial testing equipment, plastic packaging, construction fasteners, and welding supplies are all in its product portfolio. It makes very little under the company’s brand name, though. Illinois Tool Works is a true conglomerate of several different businesses that not only operate independently of one another, but each of which operates under its own moniker.

Image source: Getty Images.

This entrepreneurial-minded model works, too. Illinois Tool Works is consistently profitable and a reliable grower.

More important to interested investors, this constant cash flow has allowed the company to raise its dividend payment for 62 consecutive years. And by more than a little. Over the course of just the past decade, its quarterly per-share payout has improved from $0.55 to $1.61. That’s annualized growth of a little more than 11%, easily outpacing inflation during this stretch.

Affording these payments isn’t a problem, either. Last year’s total payout of $6.22 per share was more than covered by the company’s full-year GAAP earnings of $10.49, extending a long-standing payout ratio that’s hovered around a comfortable — and sustainable — 60% for several years now.

No pizzazz, but plenty of performance

And this begs the question: Why is this solid dividend stock down 12% from its mid-February peak?

It’s for many of the usual reasons you’d expect, like growth headwinds, economic uncertainty, and valuation concerns. Mostly, though, rather than an indictment of the company’s prospects or the stock’s valuation, the slide since then is just a right-pricing of the stock following its early February surge. Analysts still expect continued top-line growth of a little more than 3% this year as well as next to drive considerably faster per-share earnings growth, as has been the case for years now.

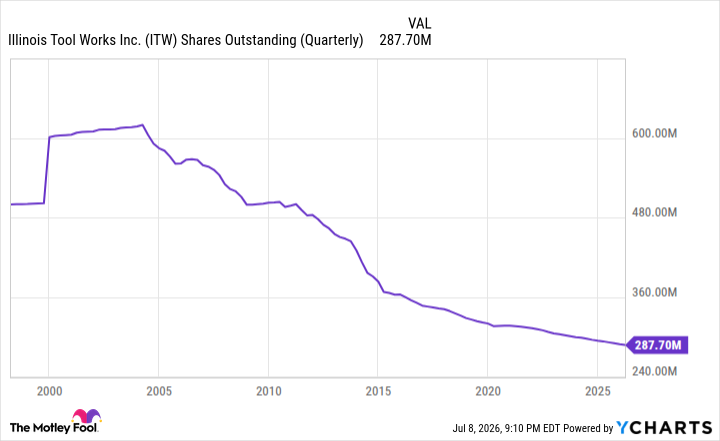

ITW Shares Outstanding (Quarterly) data by YCharts

See, Illinois Tool Works has also been steadily buying back its own stock since 2004, more than halving its outstanding share count over that period. These stock repurchases aren’t apt to end anytime soon. The $76 billion company expects to spend $1.5 billion buying back its own stock this year alone.

Today’s Change

(0.14%) $0.38

Current Price

$265.48

Key Data Points

Market Cap

Day’s Range

$263.55 – $267.98

52wk Range

$238.82 – $303.15

Volume

1.2M

Avg Vol

1.4M

Gross Margin

43.65%

Dividend Yield

2.43%

No, it’s not a sexy growth company in a high-flying industry like artificial intelligence. It’s relatively boring, in fact, and slow moving.

For income investors in need of reliable income and inflation-beating dividend growth, though, this often-overlooked outfit offers it in droves. The recent weakness is a buying opportunity, letting you in at a relative low point in a long-term uptrend. Don’t overthink it.